Most fund documents also contain often highly complex formulas covering escrow arrangements and clawbacks. These can vary significantly in their construction and impact, but in simple terms, they are mechanisms that require the GP to reserve some share of the carried profit it receives (via an escrow or a similar set-aside mechanism) to provide sufficient resources to allow LPs to claw back a portion of the carried profit previously paid to the GP if it has turned out to represent an excess share of the fund's gross profits, that is, more than the 20 percent the GP is typically due. Clawback provisions are crucial for protecting LP interests and ensuring fair profit distribution.

As noted above, under most funds' terms, a GP becomes entitled to carried profit once the LPs' drawn down investment plus the accrued preferred return on it has been returned and paid, respectively. Understanding the role of clawbacks is essential in a comprehensive analysis of private equity fees and costs. Investors should be aware of these provisions and their implications. The drawn-down investment is the key point of distinction. It is perfectly possible, in the event that a fund's earlier investments produce big wins, for those proceeds to cover the then drawn-down investment and preferred return, therefore giving the GP entitlement to carried profit, while a portion of the fund's original funding remains uncalled and available for new investments. If in turn the balance of the original funding goes thereafter into investments that prove to be loss-making, the fund may not have sufficient cash flows to repay the drawn-down investment and preferred return associated with them.

Understanding Clawback Provisions in Private Equity

In those circumstances, through carried profit earned on the earlier, profitable investments, the GP could have received more than 20 percent of the fund's ultimate gross gains, given that the LPs have had to absorb the loss of the remaining uninvested funding by themselves. Clawback is a mechanism designed to address such situations. If, however, some of the carried profit earned earlier by the GP has been placed in escrow, the LPs have a readily accessible means to seek repayment of carried profit and to try to bring the balance of profits earned back into 80/20 alignment via an exercise of clawback provisions. Certainly, moving to recover funds held in escrow is far easier than pursuing individual members of the GP to repay carried profit distributions they received directly, which may well have been spent before the over-distribution scenario arises.

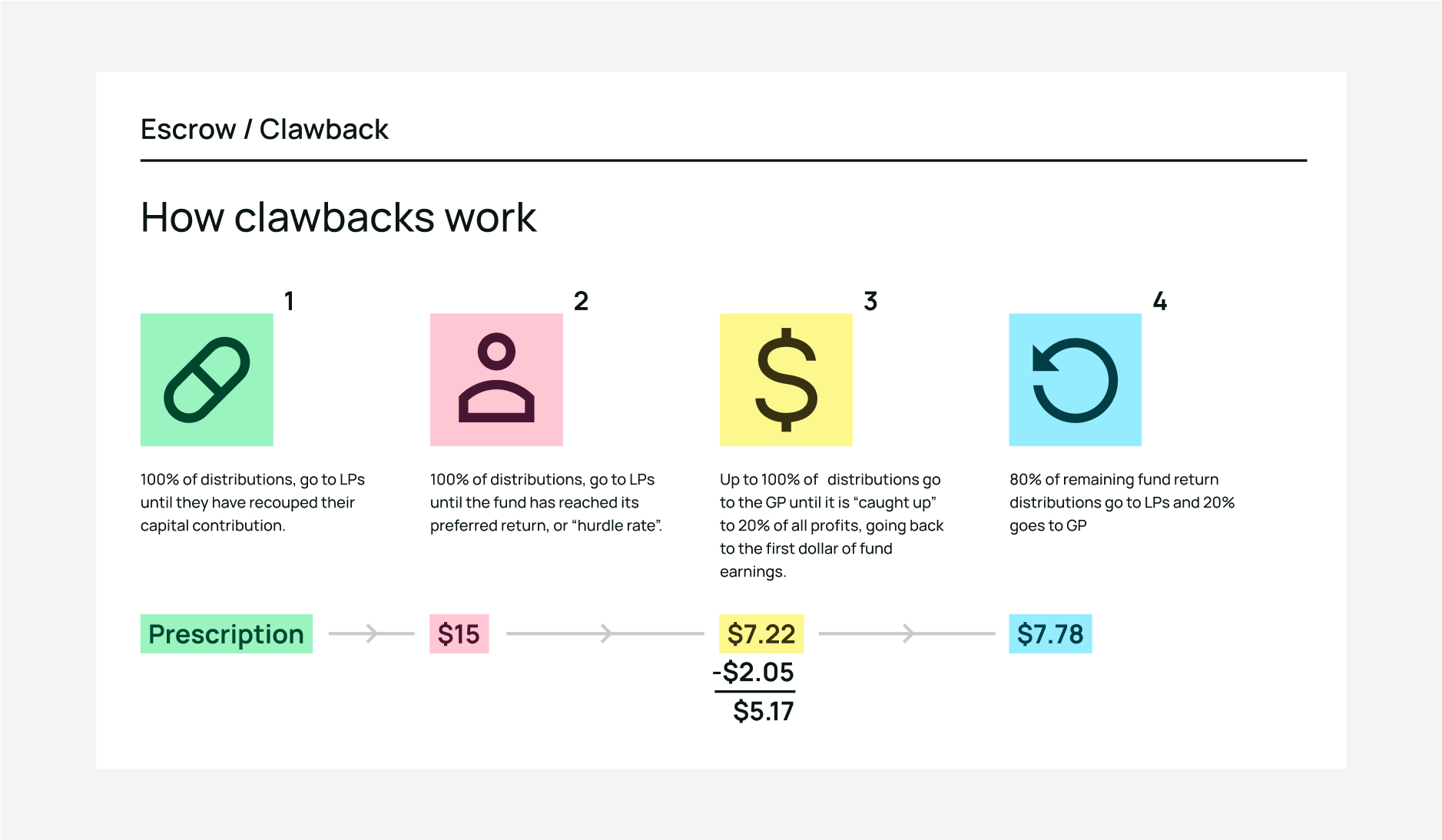

Clawback in 4 Simplified Steps:

1. Carried Profit Distribution: Once LPs' investment and preferred return are covered, the GP gets their profit share, typically 20%. They might receive this if early investments yield high returns, even if some fund funding remains uninvested.

2. Escrow Mechanism: A part of the GP's carried profit is reserved in an escrow to cover potential future profit discrepancies.

3. Potential Losses: If later investments in the fund result in losses, the GP's previously received carried profit might exceed their 20% entitlement of the total fund profits.

4. Executing Clawback: If the GP's share surpasses 20%, LPs can "claw back" the excess from the escrow to maintain the intended profit distribution, usually 80/20 between LPs and GP.

The Rise of Clawback Provisions: From Boilerplate to Essential Term

For many years, these lesser economic provisions did not attract as much LP interest in negotiations of terms and were often regarded as quasi-'boilerplate', covering scenarios with a very low probability of arising. This changed in 2001-02, when many previously high-flying US venture companies with seemingly stratospheric returns crashed rapidly after the technology, media, and telecommunications (TMT) boom turned to bust. This period highlighted the importance of clawback provisions in protecting investor interests. Many such funds had recorded monumental gains on earlier investments benefiting particularly from IPOs issued via the gravity-defying NASDAQ, and had paid out carried profit to their GPs of considerable scale.

A parallel can be drawn with the way bank fees are scrutinized. While seemingly small, these fees can accumulate over time, impacting overall returns. Similarly, the absence of strong clawback provisions can lead to a significant erosion of investor profits in certain scenarios.

Unfortunately, however, later investments that missed the window often led to catastrophic losses, leaving funds as a whole underwater and the LPs seeking redress, via escrows and clawbacks, from GPs that had received - in light of time - excess carried profit rewards. Clawback provisions gained prominence during this time as investors sought ways to recoup losses. To a lesser extent, these unfortunate scenarios also played out in buyout funds that suffered unusually high levels of loss-making and written-off investments (relative to historic norms) during the GFC and its aftermath. The GFC further reinforced the need for robust clawback mechanisms in fund agreements. Therefore, as theoretical estimations became practical experiences for LPs in these circumstances, some of it hard and costly, since then 'what if' terms such as escrows and clawbacks have received far more attention, across funds of all types, not just venture companies .